LTCM vs Three Arrows — When Genius Failed?

It is a tough time for most people in the crypto industry. Three Arrows Capital (3AC) went under, looming credit contraction crisis, and FED pivoting between hawkish and dovish sentiment doesn’t make things any easier. Daddy Jerome Powell could speak for 10 minutes and takes the entire market together with him, like he did yesterday after the Jackson Hole Symposium.

The similarity between 3AC and LTCM is simply uncanny, in that both funds are arbitrageurs at heart, and specializes in stats arb. As a buy side quant trader myself, I could appreciate these trades to the brim. Cash and carry in the cryptocurrency market for instance could capture a DV01 (or BV01, as in Bitcoin Value) basis of up 40% just last year in 2021 during the bull market, all while remaining perfectly delta-neutral and taking no directional bets. For LTCM, they do not take speculative directions of any kind, and profiting off the mispricing in the market. LTCM had a leverage ratio of 25:1, with an AUM of $5B in 1997, which is worth about $8B in 2022.

The insane amount of leverage used by LTCM was only possible as the bond market has much lower volatility in general.

Applying that amount of leverage in the cryptocurrency market will rain havoc for multiple lifetimes and over, plus getting all sorts of rekt. It is not uncommon for the cryptocurrency markets to be trading at 100–200% annualized volatility. Currently, during a bearish or side-ways market, volatility is lower at around 60%.

Three Arrows had a NAV of $10B at the time of implosion. The only difference is that, the FED had occastrated a bailout of $3.6B for LTCM from 14 other banks to cover the margin calls back in 1997. Without any form of bailout or assistance, 3AC went down and the crypto market went into a credit crisis.

A lot of creditors such as Voyagers, Genesis pretty much had a hole punctured in their sheets. Gaining access to credit undercollaterized, and sometimes even with no collateral was possible for a hedge fund with such a long running good reputation, just like LTCM. Needless to say, the access to easy credit is seriously obscured post-3AC implosion. That being said, while the lenders from the traditional finance are facing troubles getting their fair share of reimbursement, the users who participate in lending out their capital in decentralized finance through protocols such as Aave and Compound had zero hiccups and downtime. The code is law nature of smart contracts held up its end of the bargain and secured the inventories of the creditors.

This is showing great resilience and promise for the future of lending business. One caveat of the lending protocols in the DeFi space is capital efficiency, whereby all loans require an overcollaterized baskets of assets, but it still provides liquidity for most use cases.

Those guys from TradFi are also slowly stepping foot into the technological disruptive crypto market. Although they still have a plethora of compliance nighmare and regulatory constraints to deal with, the trend is brewing. Decentralization shows resilience, blurring the lines between DeFi and TradFi.

Taking us back to comparing and contrasting between the two genius funds, LTCM had only two kinds of trades, which are relative value arbitrage and convergence trades.

Convergence Trades

Convergence trades involve two assets that will converge with time and maturity.

One example would be the on-the-run vs off-the-run US government bonds, which are essentially bonds with the same maturity and supposedly same yield but released at different times. The liquidity disparity between the two have created an illogical yield spread. Off-the-run bonds are usually under-priced, hence the trade is to take a long position in them while simulatenously shorting the on-the-runs treasury bonds, taking no speculative risk and exposure in the direction of the interest rates.

Relative Value Arbitrage

Relative value trades are slightly more speculative in nature, betting on the mean reversion property of two strongly correlated or cointegrated assets.

One example would be the Italian treasury bonds vs Italian corporate swaps, in that the fixed rate Italian swaps curve was below the Italian yield curve. In other words, investors were more bullish over Italian corporate bonds than government bonds. This was not logical, such trades are an easy decision if the phenomena is picked up by the research team. Betting on them to converge relatively, or even flipping directions, the trade is to long the Italian treasury bonds, while hedging with the same amount (presumably beta or dollar neutral) of exposure in Italian swaps. The non-trivial default risk of the country and the companies are hedged with insurance.

LTCM also bet on volatility spreads, merger arbitrage and so forth over time which are higher risk in nature, which had led to the eventual downfall of the fund during and throughout the 1997 Asian Financial Crisis in aftermath of the Russian Government bond defaults, and correspondingly devalued the Ruble. For more of their trades and timelines, I suggest reading this book When Genius Failed: The Rise and Fall of Long-Term Capital Management, which is my favourite book to date simply because everything is very relatable, and able to get a non-superficial glimpse at the markets of the 90s.

As for 3AC, the catastrophic and destructive implosion of it actually started around the beginning of the year 2021 through a series of events:

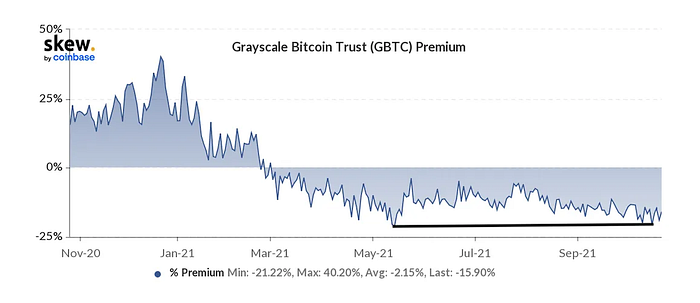

- Grayscale Bitcoin Trust (GBTC)’s NAV started trading negative to the underlying asset, in this case Bitcoin (2021)

- LUNA implosion and UST Depeg (2022)

- ETH 2.0 Merger Arbitrage (2022)

Grayscale Arbitrage

GBTC is nothing but an investment product that tracks the bitcoin price which can be purchased through a regular brokerage account. Due to a skewed supply and demand, GBTC has been trading at a premium to spot. 3AC was betting on the sustainability of the premium that has been existing for the longest time, until around the March of 2021.

It might make sense for some groups of people to own GBTC instead of bitcoin spot. US retail investor benefits from purchasing GBTC through their 401(k) accounts without needing to pay for income tax. Besides that, some institutional investors such as Morgan Stanley who could not hold bitcoin spot due to regulatory concerns could gain exposure to cryptocurrency through owning shares from this investment trust.

One can subscribe to GBTC at the market price (USD subscription), or through pledging in BTC (in-kind subscription) for a 1000:1 subscription service. The subscriptions will be locked up for 6 months before it is released to the secondary market. This lock up period used to be for a whole year before 20th of April, 2020. Only accredited investors can subscribe to GBTC. The retails can only salvage whatever the big boys are dumping in the secondary market post release. Rekt. Hence, the game is to bet on the spread to be sustainable through the entire lock-up period. So what’s the game plan for this arb?

- Borrow BTC

- Pledge the BTC to Grayscale to issue GBTC shares (1 GBTC = 0.001 BTC)

- Wait for 6-months of vested period

- Dump the shares at market price. Note that we subscribed to the shares at NAV, hence taking home a fat paycheck.

- Rinse and repeat

At some point, the spread was at 120%, or 240% annualized return in between 2017 and 2018 for a supposedly “risk free” convergence trade. The spread was still well around 20 to 40% throughout 2019 and 2020. The profit was too good to miss. 3AC went on a step further by leveraging on this trade. Grayscale Investment and Genesis are both subsidiaries of a venture capital Digital Currency Group (DCG). 3AC, speculatively can lever up by borrowing BTC with bare minimum collateral (possibly zero) from Genesis, and also pledging the minted GBTC shares to borrow USD again. What’s in it for the investment trust? They make 2% management fees. Some miners may also be willing to act as counterparty to this entire game by lending 3AC some BTC to lever up the trade to squeeze the premium, all while taking a piece from this lucrative “risk-free” arb. Or so we thought.

Now, the shares of the largest bitcoin investment vehicle in the world is trading negative to the underlying asset, the trade has now gone under. The discount has even widenened to -35% recently. There’s simply just too much shares on the market than people are willing to buy. When GBTC was the only game in town, the market demand far outweights the supply, hence the premium. As other bitcoin ETF becomes available, the supply outstripped demand and so the GBTC shares flipped to a discount to NAV. The shares are non-redeemable for BTC hence the only way to get rid of the inventory is by selling the GBTC shares in the open market. This would incur a huge loss. The only salvation now as suggested by the CEO of Grayscale Investments, Michael Sonnenshein is by converting the investment vehicle to a bitcoin spot ETF so that the ETF arbitrageurs can arb the hell out of it, thus closing the spread and saving the day for grayscale investors. The SEC definitely is not very happy about it.

A -35% discount would amount to a loss of 105% + 6% management fees + borrowing interest rates at 3x leverage. That drawdown should blow everything up. The silver lining is that, presumably at this stage, the loss is only unrealised. If Grayscale can pull the entire bitcoin spot ETF conversion fiasco into reality, it saves the day. Hence, they didnt have to file for bankrupcy (presumably) in 2021 even if they sold the universe on that trade as long as all the counterparties are willing to hold the inventories and not liquidate 3AC’s position. It is also not in their best interest to liquidate the 3AC fund and take the risk of 3AC going down and taking their capital together with it.

LUNA Implosion and UST Depeg

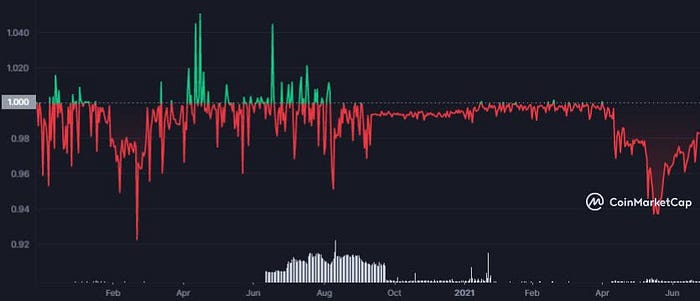

This has got to be the greatest trade in the cryptocurrency history thus far. A trade that took my favourite ponzi scheme, UST and LUNA down and jeopardized the entire cryptocurrency market, especially the stables. Most things pegged were under serious duress, USDT, stETH, TOMB, CVX etc. We will talk about stETH in great detail later. That LUNA collapse and the UST depeg was a George Soros moment indeed. Remember how he created bank runs and attacked the Bank of England and also in the Asia markets? To put things into perspective, LUNA was around 50 billion in market cap, and UST was around 20 billion when it crashed to zero. When the investment bank, Lehman Brothers went under in 2008, it had approximately 60 billion in market capitalization, which is worth about 75 billion in 2022. Morgan Stanley and Goldman Sachs are worth around 100–150 billion as of today. This LUNA implosion was an event the size of the Lehman crisis back in 2008. We are now definitely living off the pieces that is left in the cryptocurrency industry. LUNA and UST was a ponzi scheme I felt strongly about. So I definitely take no joy in their implosion.

Kyle Davies, one of the founders of 3AC has mentioned pledging 200M worth of cash into a LUNA token sale back in February 2022. The beta play was all sorts of rekt for 3AC and it literally went to zero. However, speculatively, a high risk beta play was not the only culprit. Su Tzu and Kyle Davies were both arbitrageurs at heart. There’s a protocol that allows users to earn 20% “risk-free” in UST by staking UST. The protocol was only able to generate 10–12% of profit through the borrowers, which was incentivized by the protocol’s token ANC, and also staking the funds for more yields. Hence, someone had to fund the remaining 8%. Thank you LUNA Foundation. The plan was to sustain the high yield to attact a large enough user base, while buying time for the team to figure out a way to sustain the yield. At some point, Luna Foundation Guard (LFG) had bought 1.5B worth of BTC (presumably 42k per BTC) to defend the peg. That should whet some appetites. Since UST is pegged 1:1 to USD, this trade is tempting. The peg was supposedly well-defended at least for the next forseable few months with good reserve in the LFG and team. Hence, printing USD this way is a hard miss.

- Borrow USD

- Convert USD to UST 1:1

- Stake UST into Anchor Protocol (it’s like a commercial bank but in crypto)

- Interest bearing aUST received as a receipt of deposit

- Collaterize aUST for more UST in Adacadabra

- Rinse and repeat

Again, like no other. It is only logical to pledge the aUST into more liquidity, and redo the trade mutiple rounds to leverage up. Bump those rookie numbers up. Only, this time aUST can be levered up much easier through a DeFi protocol, Adacadabra using their Degenbox Toolbox. aUST can be flipped for UST. If the 1:1 peg is stronk, the leverage factor can be pretty high. 3AC also did not have to use their own USD cash flow. They could very well use borrowed funds and have their first round of capital leverage in the form of borrowed USD. Although, a UST depeg was not unheard of, but it was well defended at every single attack, except until it wasn’t. The bank run was so well-executed I had goosebumps. Let’s bite the bullet like music to your ears.

UST is linked to LUNA like sisters, in that $1 UST is always equivalent to $1 worth of LUNA. When UST < $1, arbitrageurs buy $1 UST, burn it and mint $1 worth of LUNA, and sell the LUNA for a small profit and vice versa when UST > $1. This way, the peg can be maintained, except of course until a “death spiral” occurs, where the act of selling LUNA necessitates more LUNA being minted for each UST burned, creating a hyper-inflationary loop in LUNA’s supply.

The attacker made 800M and took down a strong competitor on this masterplan (assuming the rumours are true).

- Adversarial attacker(s) (rumoured Blackrock and Citadel) borrowed 100k units of BTC from Gemini, so that is approximately $4.2B worth of short position

- The attacker accumulates $1B in UST via OTC, speculatively from Do Kwon or LFG themselves, as buying UST in the open market at such volume will move the markets. This also drains their UST liquidity

- LFG removes $250M of liquidity from Curve 3pool liquidity in anticipation of 4pool migration post Curve war

- Attacker spends $350M UST to drain the curve liquidity, selling UST to flood the market with it

- UST depegged to ~ $0.97 USD/UST. LFG started selling BTC for liquidity to defend the peg, causing a downward pressure on BTC.

- Attackers uses the remaining $650M UST to drain the liquidity in Binance.

- People started to panic exit, creating cascades of forced selling in both LUNA and UST

- BTC downward pressure on-going and eventually LFG’s bullets were empty. CEX also suspends withdrawals. UST is now trading at 60 cents. BTC nuked to sub 30k. LUNA and UST went into the “death spiral”

- Attacker made $900–1000M on the short position on BTC, minus the losses of $350M UST curve dump, and $650M Binance dump due to slippage. Assuming 3% curve depeg, that’s only $10.5M lost, and assuming CEX dump was done at 80 cents, that’s $130M of losses. Net profit of about 800M.

Blackrock and Gemini had all the motivations required to pull this trade off as Blackrock is a large investor for Circle, which is the issuer of another stablecoin, USDCircle (USDC). Gemini is also incentivised to capsize another competitor to make room for their very own, GeminiUSD (GUSD), all of which are supposedly pegged 1:1 to USD fiat.

Depending on 3AC’s leverage factor, if their size if huge, that would have contributed a lot to the depeg as they sell their UST back to USD at significant losses at a supposedly “risk-free” interest rate arbitrage.

As Arthur Hayes has also previously mentioned, this shitty bond yield is nothing short of rare, why are we even surprised that it blew up.

ETH 2.0 Merger Arbitrage

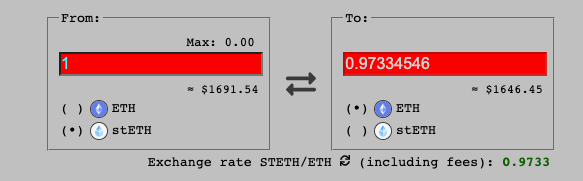

There are various ETH staking ecosystems to participate in the PoS version of Ethereum. One such is through the Lido Finance protocol. The Ethereum 2.0 Beacon Chain requires stakers for validation purposes, and Lido Finance provides an infrastructure that allows retail to have a skin in the game, while at the same time, creating liquidity for the staked ETH, coined stETH. This stETH is therefore free to use for other DeFi yield farming activies, while your ETH is locked for PoS. stETH is redeemable for ETH 1:1 post-merge, so the risk is well mitigated. But what’s the catch? That stETH can maintain its peg, and that the merge actually happens, otherwise your ETH stays locked. Staking ETH is the only way to generate rewards from on-chain transactions after the merge. One also gets staking rewards for locking up your ETH through Lido Finance. There’s the incentive to participate in this play.

For our arbitrage trade, the story is never complete without the use of leverage to screw things up. Hence, there goes

- Borrow ETH

- Stake ETH for stETH in Lido Finance for 4% return

- Pledge stETH as collateral in Aave to borrow more ETH

- Rinse and repeat

Due to the aforementioned LUNA fiasco, fear started spreading like wild fire which started depegging most things stable. At some point, stETH was down to sub 0.9 ETH per stETH. Currently, stETH is still trading at a slight discount to ETH.

The good thing about cryptocurrency is the transparency. Everything is recorded on-chain. The people has labelled this wallet/transaction as one of the 3AC’s public address, who is selling stETH back to ETH and also unwinding AAVE loans, obviously at a loss.

With three cascading events, 3AC had to file for bankcrupcy. They did well, but the market was too cruel.

So now that stETH is still trading at a discount, what’s the new game plan? Earning the staking rewards was not the only lucrative interest rate arbitrage in town no longer for ETH. We can also participate in a convergence trade, betting on the spreads between stETH and ETH.

Assuming the merge actually happens, and is tentatively planned to be around 15–16th September 2022, depending on when it reaches the glory technical details that I am going to spare, this is a pretty easy trade. stETH a.k.a ETH futures that is expiring on 15SEP2022. Hence, this is a futures term structure that is trading at a backwardation.

The beauty of DeFi is data transparency. The backwardation is caused by a larger influx of stETH into the market as traders flee a potential depeg event. This is not too logical. The painful event of UST depeg was still over the heads of a lot of people. Since stETH is mispriced, and that this spread will close upon the merge (redeemable 1:1), as long as capital availability and efficiency checks out, this can be a pretty good arb opportunity if well executed.

Currently, the ETH term structure in centralized exchanges are trading at a deep backwardation. This is in anticipation of a successful merge, and the possibility of a hard fork of POW ETH, and also a rising demand for spot to qualify for more airdrops. Spot were purchased, and futures are used to hedge the deltas. The spot demand is driven by the fundamental change in Ethereum post merge, coined “triple-halving”, which is usually a bullish case, just as the bitcoin-halving events, where the supply will be reduced post-event. At the same time, participating in the merge requires spot. Hence, even during such a bearish market, ETH is doing decently well.

One strong indicator that this time, the merge will happen is through the lens of the miners. Some are scared shitless for the possibility going out of business. Hence, POW ETH hard fork is proposed. If the merge actually results in a hard fork, POW ETH is a split that could be immediately sold for profit, assuming the general consensus of supporting POS ETH, except of course for miners who does not wish to see their mining rigs go lame. BTC has been unperforming ETH lately due to such a highly anticipated event.

Arthur Hayes is extremely bullish and categorized the merger situation into 4 different scenarios, depending on FED and the success of the merge, with a positive expected value of $2815. Very well appreciated calculations but in my opinion, the likelihood of post-event dump could not be ignored, especially if the contracts are trading at a deep backwardation. Should the event goes through, traders may unhedge and sell the spot delta exposures, driving the term structure back into a weak contango or slight backwardation, like the current case for the market leader, BTC.

During the BOBA airdrop event just a few weeks earlier, the final few days and hours were insane with never seen before funding rates and basis. 1000% annualized funding rates, few hundred percentage points of basis in FTX, post event dump of OMG and BOBA tokens were noticable. Other exchanges had to modify their cap on funding rates to fit the large hedging demand on derivatives. That being said, Ethereum is like no other shit coin. Hence, it is also not a stretch to justify the bullish case for Ethereum.

Post-Mortem Reflections

Delta-neutral trades which are supposedly “risk-free” are just margin calls that are dormant at the mercy of the market. As Charlie Munger always says, There is only three ways a smart person can go broke: liquor, ladies and leverage. Three very important “frenemies” of life indeed, how do you even strike a balance between those three 😝